This is the biggest automotive news around the globe this 2019 and after three days of the final signing, the global automotive market is still whispering about this collaboration which creates an automotive group that is larger than General Motors and is the 4th largest in the world. However, there is little enthusiasm in Malaysia since most of the Fiat Chrysler group brands are no longer in Malaysia. Brands like Lancia, Fiat, Jeep and Alfa Romeo have long gone from our shores and with this merger there is little hope of their return for many reasons.

The biggest reason being our shrinking automotive market, while our neighbours are growing and getting stronger. Then there is the economic slowdown in our automotive market due to the stalling of our National Automotive Policy which has been in cold storage for more than a year.

More can be mentioned but best to leave it for now.

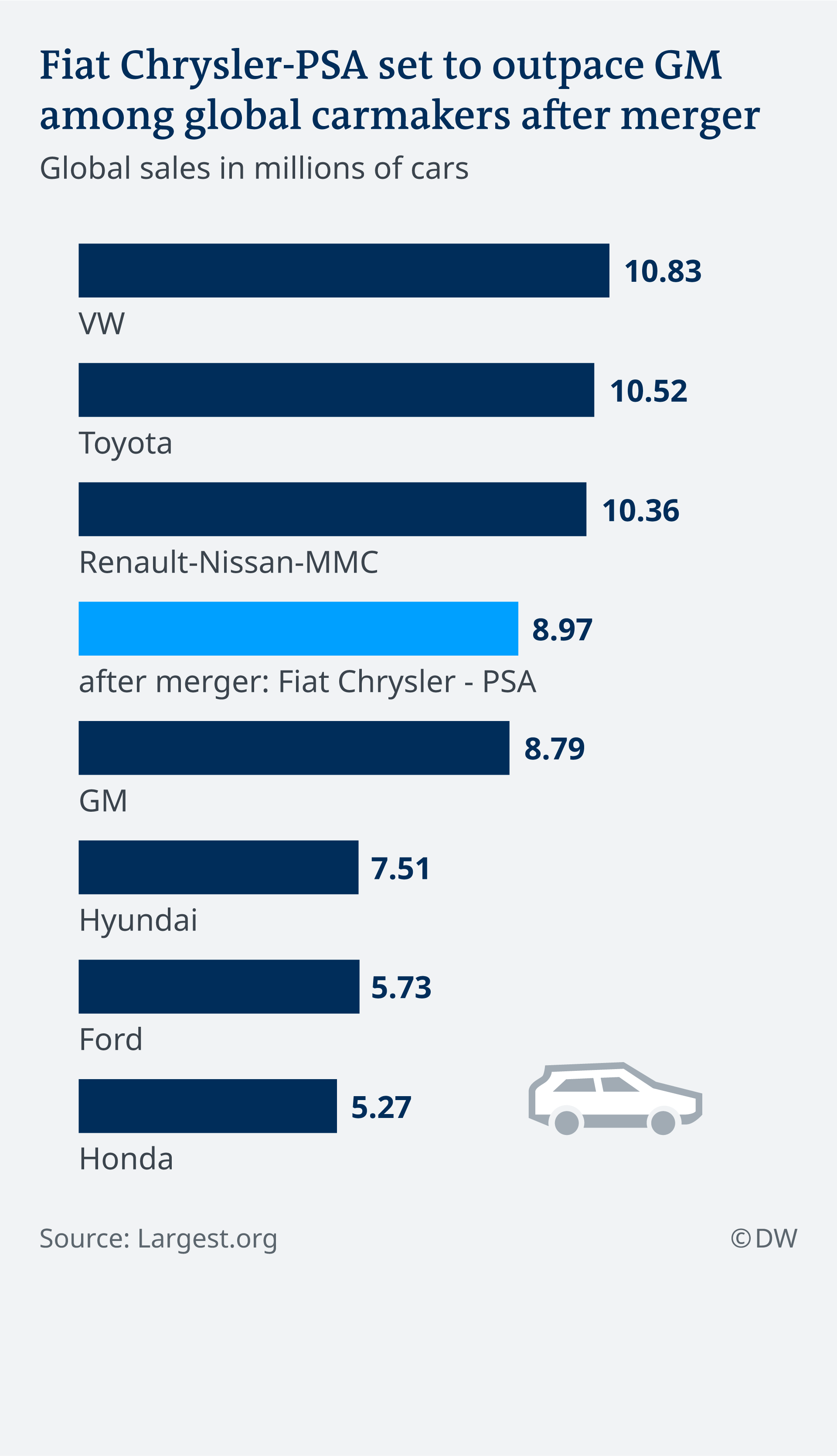

PRESS RELEASE: This new combined automotive group will be the 4th largest global OEM by volume and 3rd largest by revenue with annual sales of 8.7 million units and combined revenues of nearly €170 billion.

This is not surprising news as in recent years a number of large alliances have formed in the automotive sector to create large groups to produce better vehicles at lower operating costs.

Platform sharing, talent sharing and vendor reductions have all been done to produce better vehicles at possibly lower prices. However, it has not always been to the benefit of buyers as we have seen with the Volkswagen Groups quest to be global No.1 which they have been for the past 4 years at a cost of diesel-gate and after sales issues that have plagued owners globally. Then there was the Nissan-Renault Alliance that created a major scandal.

Still, the FCA-PSA merger looks promising as PSA has platforms and engines for the fast growing Asian region and PSA needs FCA to return to North America where it has no presence.

Fiat Chrysler Automobiles and Peugeot S.A have just signed a binding Combination Agreement providing for a 50/50 merger of their businesses to create the 4th largest global automotive OEM by volume and 3rd largest by revenue. The proposed combination will be an industry leader with the management, capabilities, resources and scale to successfully capitalize on the opportunities presented by the new era in sustainable mobility.

With its combined financial strength and skills, the merged entity will be particularly well placed to provide innovative, clean and sustainable mobility solutions, both in a rapidly urbanizing environment and in rural areas around the world. The gains in efficiency derived from larger volumes, as well as the benefits of uniting the two companies’ strengths and core competencies, will ensure the combined business can offer all its customers best-in-class products, technologies and services and respond with increased agility to the shift taking place in this highly demanding sector.

The combined company will have annual unit sales of 8.7 million vehicles, with revenues of nearly €170 billion3, recurring operating profit of over €11 billion4 and an operating profit margin of 6.6%, all on a simple aggregated basis of 2018 results5. The strong combined balance sheet provides significant financial flexibility and ample headroom both to execute strategic plans and invest in new technologies throughout the cycle.

The combined entity will have a balanced and profitable global presence with a highly complementary and iconic brand portfolio covering all key vehicle segments from luxury, premium, and mainstream passenger cars through to SUVs and trucks & light commercial vehicles. This will be underpinned by FCA’s strength in North America and Latin America and Groupe PSA’s solid position in Europe. The new Group will have much greater geographic balance with 46% of revenues derived from Europe and 43% from North America, based on aggregated 2018 figures of each company. The combination will bring the opportunity for the new company to reshape the strategy in other regions.

The efficiencies that will be gained from optimizing investments in vehicle platforms, engine families and new technologies while leveraging increased scale will enable the business to enhance its purchasing performance and create additional value for stakeholders. More than two-thirds of run rate volumes will be concentrated on 2 platforms, with approximately 3 million cars per year on each of the small platform and the compact/mid-size platform.

These technology, product and platform-related savings are expected to account for approximately 40% of the total €3.7 billion in annual run-rate synergies, while purchasing – benefiting principally from scale and best price alignment – will represent a further estimated 40% of the synergies. Other areas, including marketing, IT, G&A and logistics, will account for the remaining 20%. These synergy estimates are not based on any plant closures resulting from the transaction. It is projected that the estimated synergies will be net cash flow positive from year 1 and that approximately 80% of the synergies will be achieved by year 4. The total one-time cost of achieving the synergies is estimated at €2.8 billion.

Those synergies will enable the combined business to invest significantly in the technologies and services that will shape mobility in the future while meeting the challenging global CO2 regulatory requirements. With an already strong global R&D footprint, the combined entity will have a robust platform to foster innovation and further drive development of transformational capabilities in new energy vehicles, sustainable mobility, autonomous driving and connectivity.

The merged entity will benefit from an efficient governance structure designed to promote effective performance, with a Board comprised of 11 members, the majority of whom will be independent6. Five Board members will be nominated by FCA and its reference shareholder (including John Elkann as Chairman) and five will be nominated by Groupe PSA and its reference shareholders (including the Senior Non-Executive Director and the Vice Chairman). At closing the Board will include two members representing FCA and Groupe PSA employees7. Carlos Tavares will be Chief Executive Officer for an initial term of five years and will also be a member of the Board.

Carlos Tavares, Mike Manley and their executive teams have a strong track record in successfully turning around companies and combining OEMs with diverse cultures. This experience will support the speed of execution of the merger, underpinned by the companies’ strong recent performances and already robust balance sheets. The merged entity will maneuver with speed and efficiency in an automotive industry undergoing rapid and fundamental changes.

The new group’s Dutch-domiciled parent company will be listed on Euronext (Paris), the Borsa Italiana (Milan) and the New York Stock Exchange and will benefit from its strong presence in France, Italy and the US.

Under the proposed by-laws of the combined company, no shareholder would have the power to exercise more than 30% of the votes cast at shareholders’ meetings. It is also foreseen that there will be no carryover of existing double voting rights but that new double voting rights will accrue after a three-year holding period after completion of the merger.

A standstill in respect of the shareholdings of EXOR N.V., Bpifrance8, Dongfeng Group (DFG) and the Peugeot Family (EPF/FFP) will apply for a period of 7 years following completion of the merger, except that EPF/FFP will be permitted to increase its shareholding by up to a maximum of 2.5% in the merged entity (or 5% at the Groupe PSA level) by acquiring shares from Bpifrance and/or DFG and/or on the market9. EXOR, Bpifrance and EPF/FFP will be subject to a 3-year lock-up in respect of their shareholdings except that Bpifrance will be permitted to reduce its shareholdings by 5% in Groupe PSA or 2.5% in the merged entity. DFG has agreed to sell, and Groupe PSA has agreed to buy, 30.7 million shares prior to closing (those shares will be cancelled). DFG will be subject to a lock up until the completion of the transaction for the balance of its participation in Groupe PSA, resulting in an ownership of 4.5% in the new group.

EXOR, Bpifrance, the Peugeot Family and Dongfeng have each irrevocably committed to vote in favor of the transaction at the shareholders’ meetings of FCA and Groupe PSA.

Before closing, FCA will distribute to its shareholders a special dividend of €5.5 billion while Groupe PSA will distribute to its shareholders its 46% stake in Faurecia. In addition, FCA will continue work on the separation of its holding in Comau which will be separated promptly following closing, for the benefit of the shareholders of the combined company. This will enable the combined group’s shareholders to equally share in the synergies and benefits that will flow from a merger while recognizing the significant value of both Groupe PSA and FCA’s assets and strengths in terms of market share and brand potential. Each company intends to distribute a €1.1 billion ordinary dividend in 2020 related to fiscal year 2019, subject to approval by each company’s Board of Directors and shareholders. At closing, Groupe PSA shareholders will receive 1.742 shares of the new combined company for each share of Groupe PSA, while FCA shareholders will have 1 share of the new combined company for each share of FCA.

Completion of the proposed combination is expected to take place in 12-15 months, subject to customary closing conditions, including approval by both companies’ shareholders at their respective Extraordinary General Meetings and the satisfaction of antitrust and other regulatory requirements.

Carlos Tavares, Chairman of the Managing Board of Groupe PSA, said: “Our merger is a huge opportunity to take a stronger position in the auto industry as we seek to master the transition to a world of clean, safe and sustainable mobility and to provide our customers with world-class products, technology and services. I have every confidence that with their immense talent and their collaborative mindset, our teams will succeed in delivering maximized performance with vigor and enthusiasm.”

Mike Manley, Chief Executive Officer of FCA, added: “This is a union of two companies with incredible brands and a skilled and dedicated workforce. Both have faced the toughest of times and have emerged as agile, smart, formidable competitors. Our people share a common trait – they see challenges as opportunities to be embraced and the path to making us better at what we do.”